You have probably run across the idea of accounts receivable factoring and accounts receivable financing. You may have wondered what is the difference between the two concepts. Both of these can be used to acquire quick working capital. However, there are major differences between the two concepts. Banks don’t normally offer true accounts receivable factoring because they will not buy unpaid invoices, but rather use them as collateral for a loan. Here are the key differences between these two methods of financing:

Factoring Companies Buy and Banks Loan

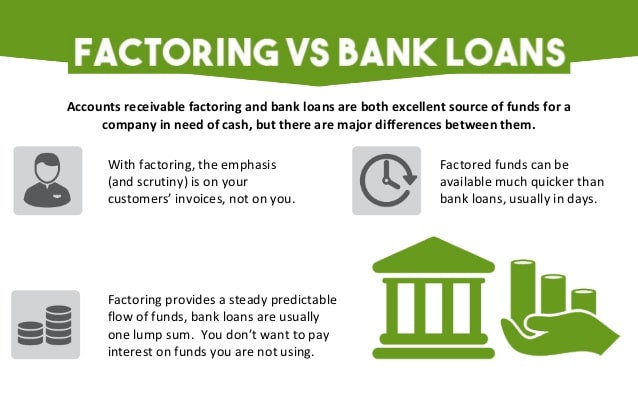

This is the primary difference between these two concepts. Banks require you to pledge the invoices as collateral for a loan while a factoring company will purchase the unpaid invoices at a discounted rate. Both the bank and the factoring company will examine your accounts receivable and decide which ones are too risky to be considered, but the factoring company is usually willing to accept greater risk. Also, since factoring is not a loan, it will not affect your debt utilization and debt-to- equity ratio. A bank loan will and it will also have a negative effect on your debt-equity situation.

Factoring Companies Pay 96% to 99%, Banks Pay Only 75% to 85%

Factoring companies will advance you 75% to 95% on the unpaid invoices that their willing to factor. They hold the remaining 25% to 5% in reserve. When your customers pay their invoices, the factoring company pays you back most of the reserve. They will keep 1% to 3% for a factoring fee. Most of the banks will loan you only 75% to 85% of the value of the invoices that their willing to accept as collateral and they will charge you an interest rate on the loan. These interest rates are typically higher than their traditional bank loans.

The Factoring Company Takes on the Responsibility of Collecting Payments on the Invoices; Banks Leave that Responsibility to You

The Factoring Company buys your invoices and now they have the responsibility to collect payments. You can now save money by not having this responsibility. If you choose to use a bank loan, the responsibility for collecting payment is still left up to you and your staff, not the bank. Also, in many cases, the factoring company will provide you credit protection. If a customer does not pay or goes bankrupt before the invoice is paid, the Factoring Company takes the hit, not you. Of course, if you go with a bank loan, there is no credit protection since you still own the accounts receivable.

In Conclusion

If you need working capital, either one of these methods might hep you. My suggestion is that you call me, Charles at Caps Funding, LLC to discuss the matter. My phone number is (803) 429-3686. Or, you can email me. I can help you weigh the pros and cons of both methods and we can come up with the best answer for you.